The Numbers Are Obscene

Micron's fiscal Q3 2026 earnings report, published June 24, reads like a dispatch from a parallel universe — unless you happen to be selling DRAM. Revenue hit $41.46 billion, up 346% year-over-year. Gross margin: 84.9%, an all-time company record, up 10 points from the prior quarter alone. DRAM revenue: $31.3 billion, up 343% year-over-year, with DRAM spot prices rising "in the low 60s percentage range" in a single three-month span. CEO Sanjay Mehrotra described the memory industry as "structurally transformed by the proliferation of AI." He is not wrong. He just omitted the part where consumers are funding the transformation — involuntarily.

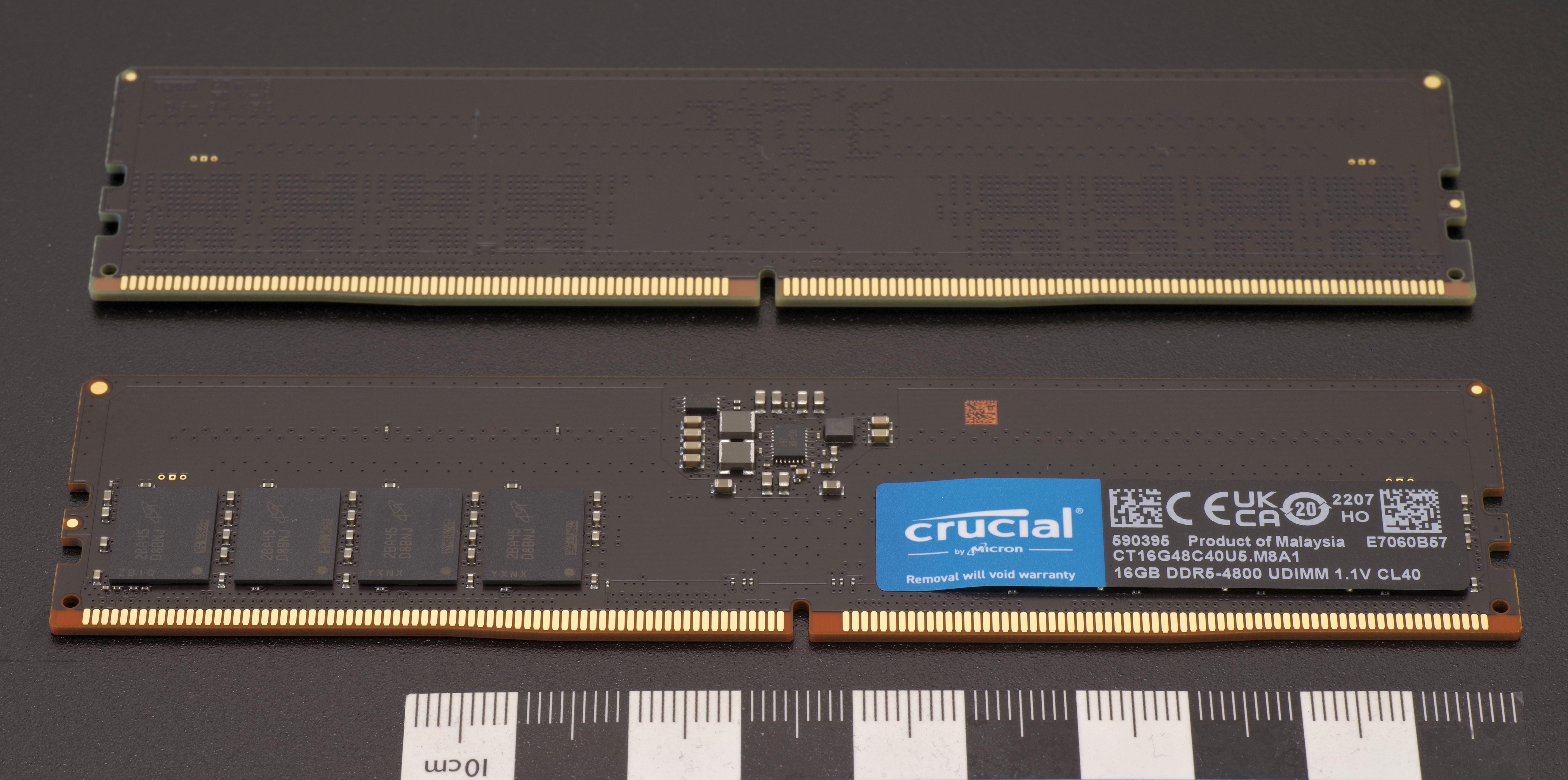

The Crucial Brand Is Dead. You Should Still Be Angry About It.

In December 2025, Micron announced the end of the Crucial consumer brand, with retail sales ceasing by February 2026. For anyone who has ever built a NAS, home server, or Proxmox node, Crucial was the default answer. Reliable binned DRAM, widely available, at non-predatory prices. Gone. Micron EVP Sumit Sadana explained the math without apology: the company is redirecting supply to "larger, strategic customers in faster-growing segments." A single HBM3E module sells for $60–100; the equivalent capacity in consumer DDR5 fetches $5–10 on the same silicon. That revenue disparity makes the decision obvious, if deeply unwelcome for the rest of us.

Six months on, the Q3 earnings call filled in the rest of the picture. Micron has signed 16 Strategic Customer Agreements covering roughly 20% of DRAM and one-third of NAND volume — $100 billion in minimum contractually enforceable revenue, with $22 billion in customer deposits already collected in cash and letters of credit. The hyperscalers building AI infrastructure have reserved Micron's production capacity for years. Consumer channels were not invited to that negotiation.

The CEO Said What He Said

Buried in the earnings call coverage was the most important data point in the report: Micron can only meet 50 to 67 percent of customer demand in the medium term. This is not a temporary hiccup. It is a structural production deficit with no near-term resolution. Micron's new Idaho fab doesn't begin DRAM production until mid-2027. Samsung and SK Hynix are on similar construction timelines. The three companies that control 90–95% of global DRAM supply have all made the same capacity allocation decision, and none of them are building themselves out of this shortage in time to matter for your 2026 or 2027 build.

HBM is consuming the wafer capacity that used to produce your DDR5. HBM4 requires approximately three times the wafer area per gigabyte compared to standard DRAM, and Micron reports HBM4 is now ramping twice as fast as HBM3E did. Over $1 billion in HBM4 revenue shipped in Q3 alone. Every wafer allocated to a data center AI accelerator is a wafer not becoming the ECC RDIMM you need for your next storage server.

What This Costs You Right Now

A 32GB DDR5-5600 kit has gone from roughly $85 at the 2025 market floor to approximately $370 at Newegg's 4th of July sale, which is being advertised as a deal. That is a 335% increase in roughly 12 months. HP disclosed that memory climbed from 15–18% of their PC bill of materials to 35% by early 2026. For a ZFS-based storage server specced at 128GB ECC DDR5, budget well over $1,500 just for memory — before you touch drives, a controller, or a case.

The loss of Crucial specifically hurts for 24/7 workloads. Their consumer sticks had excellent real-world endurance in always-on NAS environments, and their pricing was honest. The remaining consumer options — Samsung B-die when you can find it, SK Hynix A-die, G.Skill at inflated prices — are not categorically worse, but they are uniformly more expensive and less reliably in stock.

Practical guidance: if you're on DDR4 infrastructure, do not rush to upgrade. Samsung has selectively restarted DDR4 production as a supply pressure valve, and DDR4 pricing is comparatively stable. For new DDR5 builds, check enterprise decommissioning channels — RDIMM and LRDIMM DDR5 from server teardowns moves through secondary markets at meaningful discounts versus retail. And if you have old Crucial sticks in your parts bin, they are worth more than you paid for them.

Micron posting an 84.9% gross margin while their consumer brand evaporates is not coincidence. It is the rational outcome of three manufacturers controlling 95% of a critical commodity during an AI spending supercycle. Supply won't improve until 2028 at the earliest. Plan accordingly.

No RAID is a substitute for backups. And no amount of hoping the market self-corrects is a substitute for buying the memory you need before next quarter's price increase lands.

Loading comments...